The largest private investment managers and their boards rely on VRC’s team for their portfolio valuation requirements.

About VRC's Portfolio Valuation Practice Group

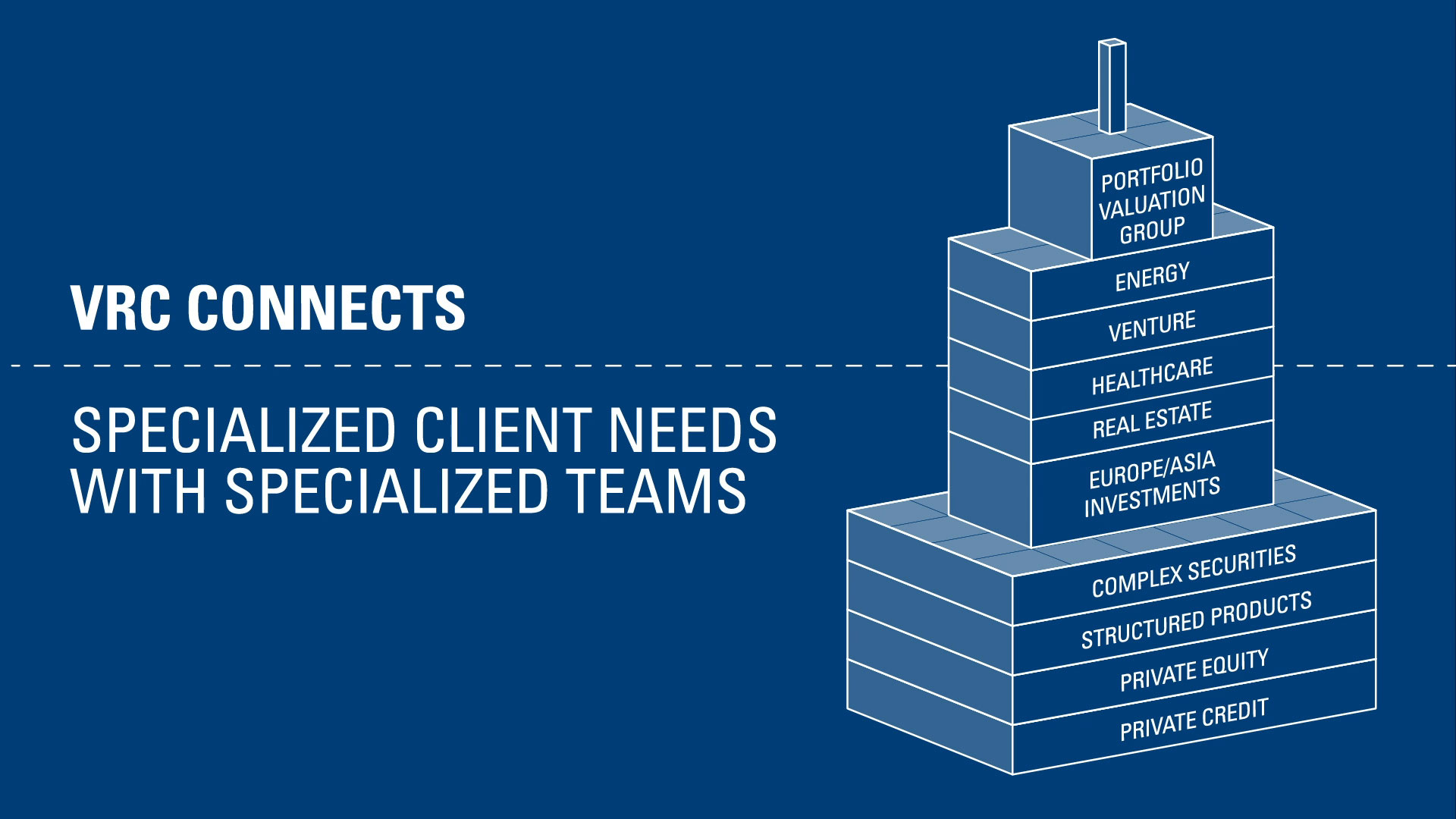

For over 100 current clients, VRC’s portfolio valuation group provides fair market values for their private investment portfolios, including equity, debt, structured credit, and complex securities.

For over 100 current clients, VRC’s portfolio valuation group provides fair market values for their private investment portfolios, including equity, debt, structured credit, and complex securities.

VRC has experience valuing thousands of private investments, a number that has grown year-over-year for nearly 20 years and counting. Organically, our practice has built itself from the ground up and boasts the largest and most experienced team when measured against its peers.

Our clients rely on our valuation services to support their internal valuations, answer questions from their auditors and enhance the comfort of their investors.

Precise Market Insights

VRC’s capital markets team manages an extensive database of proprietary market data with enhanced precision that delivers deep market intelligence via our client-exclusive VRC Market Yield Matrix.

Our intelligence reports, made for our clients, feature both emerging trends and a deep-dive of the current market, headwinds, and tailwinds and deliver actionable insights that inform short- and long-term strategies, goals, and objectives.

Your Reliable, Consistent Team

Firm-wide, we believe the importance of consistency in client relationships and service is paramount. VRC takes great pride in its industry-leading colleague retention rates, making us the reliable third-party partner clients trust.

Firm-wide, we believe the importance of consistency in client relationships and service is paramount. VRC takes great pride in its industry-leading colleague retention rates, making us the reliable third-party partner clients trust.

The fabric of our team builds upon a cultural foundation that values clear and open communication, collaboration, and innovation.

We are motivated to succeed by an ever-accessible, interconnected senior leadership team and emphasize a multi-level, proprietary internal training program that rewards hard work and dedication to one another and our clients. Evidence of this comes from the longevity of our client relationships and their satisfaction with our work product.

Why VRC?

Engaging VRC to perform portfolio-level valuations creates more efficiency in the valuation process, bolsters documentation, increases independence and transparency, and materially reduces measurement and reporting risks.

Whether we value a portfolio of general middle-market direct loans or European CLO equity, our team’s expertise will exceed your expectations. In addition to our generalist team, our specialty teams have deep experience in energy, venture, healthcare, biotechnology, real estate, and structured products.

John Czapla, CFA

John Czapla, CFA

Chairman of the Board

Head of VRC’s Portfolio Valuation Practice Group

JCzapla@ValuationResearch.com

Tel. No. (609) 243-7016

Parag Patel

Managing Director, Business Development

ParagPatel@ValuationResearch.com

Tel. No. (917) 338-5618

As the interest in private investments grows, the need for VRC's Portfolio Valuation Group’s services grows.

Our Client Base

Private equity funds

Private equity funds- Private debt funds

- Business development companies (BDC)

- Hedge funds

- Venture capital funds

- Mutual funds

- Structured credit funds

- Limited Partners

- U.S. and international pension funds

- Endowments

- Insurance companies

- Banks and other financial institutions

Industry Expertise

We provide fund managers and clients with extensive experience across many industries. We can add an independent viewpoint and an extra layer of support and transparency with more robust valuation policies that conform to best practices as a third-party assessor.

We deliver well-supported conclusions and reports that comply with the relevant reporting standards and substantiation to withstand possible scrutiny.

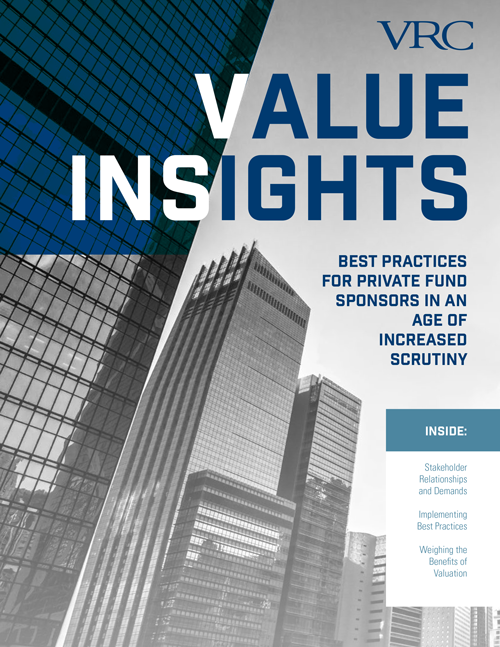

Value Insights for Private Fund Managers

Best Practices for Private Fund Sponsors

In VRC’s newest white paper, we help guide fund managers and their boards down a path of best practices to avoid unnecessary, disruptive scrutiny around valuations and withstand an inquiry with confidence.

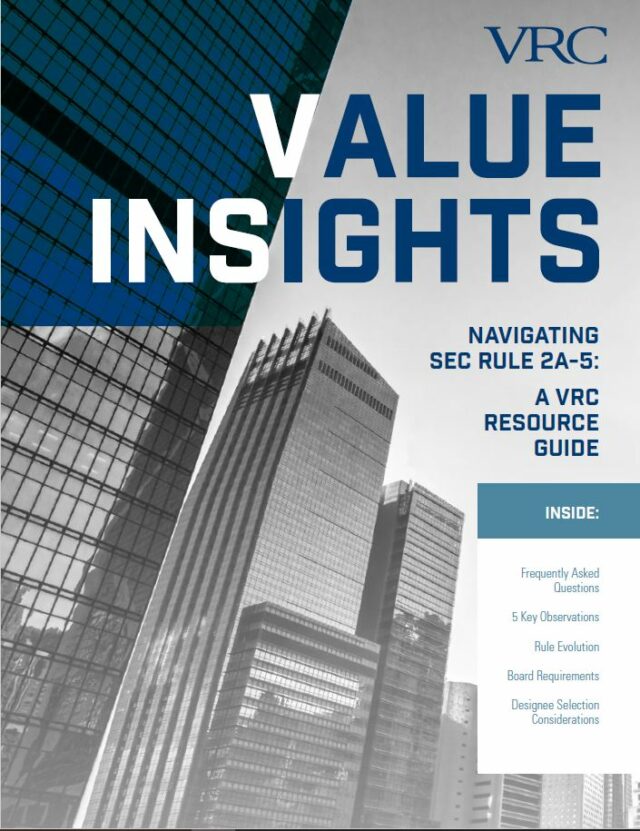

Navigating SEC-Rule 2A-5

VRC’s Rule 2a-5 Resource Guide provides the details fund managers and fund boards need to come into compliance with the SEC’s new regulations to fair value portfolio securities. Funds have until September 8, 2022, to comply with the new rule.